Readers' Choice

Popular articles

In 2019, the next conversion of pensioners’ rights began – in this case we are talking about.

Previously, similar events were observed in 2002, when everyone was keen on pension capital.

But the insurance pension is based on a new formula, because... pension points accumulated by the employee during the official performance of any official duties are taken into account.

The insurance part of the pension (SP), associated with reaching a certain age, directly depends on the amount of regular official income, time worked and amounts transferred by the insured person to the Pension Fund of the Russian Federation since 2002.

The latter are regularly indexed, and you can track them thanks to.

There is also fixed base value the insurance part of the pension, which is part of the social security account. The law that came into force in 2001 stipulates that this value is fixed, differentiated and depends on which category the pensioner belongs to. Another factor that has a significant impact is the presence (or absence) of dependents, as well as their number.

Cumulative part, caused by the onset of the age limit, depends on investment income.

SCh = PC/T+B,

Where:

Where:

Calculation of the above formula requires determining the amount of pension capital, formed before 2002:

PC = (RP-450 rubles)*T,

It is a pension that a citizen can receive before reaching the age limit, based on the relevant provisions. A mandatory requirement is work that regularly exposes life and health to danger, as well as the performance of public and government tasks.

In order to retire early, a citizen must have actual work experience, which includes an insurance and a real part. The latter requires a challenging work environment.

In order to retire early, a citizen must have actual work experience, which includes an insurance and a real part. The latter requires a challenging work environment.

Understanding the procedure for calculating early state support is achieved by considering the following example.

Sukhanov V.L. has the right to begin receiving pension benefits before reaching retirement age. His work experience is 25 years, and his official monthly income is 1.5 times the country's salary plan.

So, the calculation will take into account: the basic pension (BP) and the insurance part (SP) in points.

BP in 2019= 5334 rubles 19 kopecks.;

To determine the insurance part of the pension is required (changing annually). In 2019 this figure is equal to RUR 87.24

That is, if Sukhanov V.L. worked for 25 years, then the amount of his insurance pension will be: 25*87.24 = 2181 rub.

Total pension benefit is defined as follows:

Pension = (BP + SCH) + NP(standard state conditions provide for 16% per year, and personal desire and accumulation of interest on monthly official income - 10%).

Pension = (5334.19+2181) = 7515.19 + NP, calculated individually.

Let's assume that Sukhanov V.L. lived and worked in the Rostov region. The average salary in this region is 27,535 rubles.

Those. a citizen’s monthly income corresponds to the value 27,535 + 13,767.5 = 41,302.5, and for 1 year – 495,630 rubles. (NP = 79,300.8 rubles per year)

Maximum amount of insurance premiums RUB 212,360

NP = 79,300.8/212,360 * 10 = 3.73 points for each year worked.

25 (work experience) * 3.73 (NP) = 93.25 (points) * 87.24 (point value) = 8135.13 rubles.

Full size early pension is: 4982.9+2037.25+8135.13 = 15,506.57 rubles. monthly.

The government is gradually adjusting the procedure for calculating pension benefits.

Currently future pension calculated as follows:

K p = C l / C m * 10,

Example. The average monthly salary of a citizen is 25,000 rubles. The percentage of insurance charges is 16%. Therefore, the employer’s responsibility is to contribute to the Pension Fund: 25,000*12*16% = 48,000.00 rubles.

When compared with the maximum income set for the country in the current year, it turns out:

48 000,00/212 360 *10 = 2,26 pension points.

From size annual coefficient The volume of future payments directly depends.

If a pensioner doubts that the calculations regarding his pension provision were made correctly, then he has a direct path to the Pension Fund branch. A check, the main task of which is to control correctness, will be carried out only if the citizen expresses this request in the appropriate statement .

The Pension Fund employee is obliged to check the correctness of calculation of pension payments within 5 days and send a notification to the applicant. An erroneous calculation will automatically be brought into compliance with the law.

If you have a work record book, a calculator and certificates of average monthly income for the last 5 years, you can carry out an independent check.

Subsequence mathematical operations are as follows:

At the end, the citizen can check his calculations with the regularly transferred amount and decide how relevant it is to send an application to the Pension Fund.

The rules for calculating the amount of pension benefits are described in the following video:

Male Female

Generally established retirement age

men - 60 years old, women - 55 years old.

At this age you have the right to apply for an old-age pension.

The generally established retirement age for men is 60 years, for women - 55 years. For citizens entitled to a pension earlier than the generally established retirement age, the age at which the right to a pension arises is lower than the generally established one. Indicate the length of your expected work experience - from the start of your working career until you reach retirement age. Periods of study, childcare and military conscription are not taken into account. If your total length of service by 2021 is less than 15 years, then you will not be entitled to an old-age pension, and you (women at 60 years old, men at 65 years old) will be able to apply to the Pension Fund for a social pension, the amount of which is smaller.

0 1 2 3 4 5 6 7 8 9 10

The size of the pension under the new formula increases significantly if you postpone applying for a pension to a later date upon reaching retirement age. According to the new formula, the size of the insurance pension increases due to later retirement, that is, by applying for a pension after reaching retirement age or becoming eligible for a pension (for “early retirees”). The insurance pension will consist of the amount of a fixed payment (from February 1, 2015 - 4383.59 rubles) and the insurance part. For each year of later application for a pension, the insurance pension will increase by the corresponding premium coefficients. For example, if you apply for a pension 5 years after reaching retirement age, the fixed payment will increase by 36% and the insurance pension by 45%; if - 10 years, then the fixed payment will increase by 2.11 times, the insurance part - by 2.32 times.

Your future pension is formed only from your official salary. Here you can enter your current salary before personal income tax or the conditional average salary for your entire working life in current prices.

The higher the salary, the higher the pension will be. The main thing is that the salary must be official, that is, “white”. This means that the employer pays insurance contributions to the compulsory health insurance system for you. If you receive an unofficial salary, the employer does not pay contributions, your pension is not formed, and your length of service is not taken into account. According to the new formula, insurance premiums at a rate of 22% are paid from a maximum salary of 66,334 rubles per month.

Military service upon conscription is counted towards the total length of service. For each year of military service under conscription, according to the new pension formula, 1.8 pension coefficients and one year of insurance (non-work) experience are calculated, which is taken into account in your total length of service.

In the new pension formula, periods of leave for children (up to 1.5 years for each of four children) are counted towards the total length of service. According to the new pension formula, the following are accrued: 1.8 pension coefficients per year of maternity leave to care for the first child, 3.6 pension coefficients per year of maternity leave to care for the second child, 5.4 pension coefficients per year of maternity leave to care for the third child , 5.4 pension coefficient for a year of maternity leave to care for the fourth child.

No Yes

If you have worked in agriculture for at least 30 years and still live in the countryside, the size of the fixed payment as part of the insurance pension will be increased by 25%.

Please select your tariff.

Please indicate your gender.

According to the law, pension savings are not formed for citizens born in 1966 and older.

Enter another value for your work experience.

Please indicate your year of birth.

Enter a salary higher than the minimum wage in the Russian Federation in 2016 - 6,204 rubles.

From 2025, the minimum total length of service to receive an old-age pension is 15 years. The minimum number of earned coefficients for assigning a pension is 30. If in your answers to the questions you indicated less than 15 years of experience or the number of earned coefficients does not reach 30, then you will be assigned a social old-age pension: for women at 60 years old, for men at 65 years old. The old-age social pension today is 4,769.09 rubles per month. In addition, you will receive a social supplement to your pension up to the subsistence level of a pensioner in the region of your residence.

If you want to receive a higher pension, revise your life plans so that you have 15 years of service or more and can ultimately earn at least 30 pension factors.

Sorry, the calculator is not intended to calculate the size of pensions of current pensioners, citizens who have less than 3-5 years left before retirement.

By spending several hours a day at work every day, you build your pension.

But can you tell what the monthly payment will be?

Most people perceive their pension as a lottery: “When I live, I’ll find out how much the state valued me at.” And they try to work as much as possible without delving into the mechanisms for calculating pension payments.

According to federal law labor pension– monthly payment of funds to compensate wages to an insured person who has become disabled upon reaching retirement age or receiving disability.

Retirement age for men – 60 years, among women - 55 years. A necessary condition for receiving a pension is having a minimum established work experience.

To receive the minimum old-age pension you must work minimum 5 years. Starting in 2015, this period will increase annually by a year until it reaches 15 years in 2025.

To receive a full pension, you must have 25 years of service for men and 20 for women. In this case, the amount is formed on the basis the total number of years worked, noted in the work book.

Only official length of service is taken into account, which is logical: most of the monthly payments are made up of contributions to the pension fund, withheld from the employee’s salary.

However, these cases do not replace, but supplement the length of service when calculating insurance coverage. In other words, the work book must contain a record of work activity before or after the occurrence of one of the cases indicated above. It will also be necessary documented confirm the above circumstances, otherwise they will not be taken into account when calculating the length of service.

First of all, it is worth noting that the total pension amount is insurance and savings parts. The total contributions of employers to the pension fund are 22% .

At the same time, employees Born 1966 and older all 22% leave for the insurance part, while employees younger than 1966 year has the right to decide whether to allocate all 22% for the insurance part or give 6% on savings.

Pension accruals are calculated using the formula MF + LF, where MF is the insurance part, and LF is the accumulative part.

Obviously, for people older than 1966, the funded part is not taken into account, with rare exceptions - during the period 2002–2004, some companies credited part of pension payments to the funded part, but the percentage of such companies is negligible.

The insurance part is calculated according to the formula SCH = PK/T + B

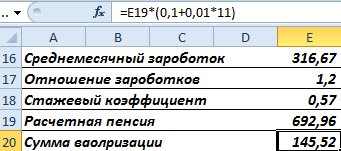

Let's look in more detail at estimated pension capital. Until 2002, the pension system was regulated a little less than not at all. Pension capital was calculated based on the total length of service and the average salary for the last 2 years of service or for any 5 years of the entire working period.

After the pension reform of 2002, the PC is formed exclusively through contributions and is recorded on the employee’s personal account in the pension fund (every citizen of the Russian Federation has an insurance number of an individual personal account SNILS). To increase the portion of the pension earned before 2002, the state introduced the so-called valorization amount. This amount is 10% of pension savings until 2002 + 1% for each full year of service until January 1, 1991.

Thus, the estimated pension capital is found according to the formula PC = PC1 + SV + PC2

From here the monthly payment will be: PK1/T + SV/T + PK2/T + B + PN/T, where PN is pension savings.

Looks a little scary, doesn't it? In fact, the formula is quite simple. And those who started their careers after 2002 do not have PC1 and SV at all.

The main innovation of this system was the input ready pension coefficient (PC). It is calculated as the ratio of employer contributions insurance premiums (SI), optionally – 10 or 16%, to the maximum allowed by law contributory salary (WW), multiplied by the maximum PC value.

In general, the pension coefficient is intended to become a new tool for accounting for human pension rights. All pension rights received up to and including 2014 will be converted into pension coefficients automatically from 2015.

Since the pension coefficient now plays the main role in calculating pensions, the new formula will look like SP = (FV x KPV) + (IPK x KPV x SPK)

Two facts immediately catch your eye: the more you work, the higher the pension and the higher your salary, the higher the pension. Well, at least everything is logical.

For those who decide to devote their lives work in rural areas, there is good news: upon reaching 30 years of experience in rural areas, the fixed fee increases another 25%(provided that the citizen remains to live there).

All these formulas, old, new systems - not everyone wants to understand the intricacies of formulas, coefficients and calculations. That is why pension calculator on the Pension Fund website, it would seem, should be the best solution for predicting your future pension.

But not everything is so simple.

The calculator interface on the Pension Fund website is really quite simple: they offer you answer 11 questions, and the system itself will calculate the predicted monthly payments based on your answers.

Next to the input fields, some items in the questionnaire have a question mark, by clicking on which you will receive a comment regarding a specific indicator.

Please note the warning in the annotation that the data as a result of the calculation should not be taken as the actual size of the future pension. This is due to the fact that all calculations are made in 2015 conditions.

You can experiment with the numbers in the columns, length of service, salary, pension option in the compulsory pension system and see how your future pension will change.

In general, the calculation system, as indicated on the Pension Fund website, is conditional character and allows you to get an approximate idea of the size of the old-age insurance pension.

If you are really getting ready to retire soon and you are interested in its size, then to calculate it yourself you will have to arm yourself with a regular calculator and understand the explanations about the procedure for calculating your future pension ( http://www.pfrf.ru/grazdanam/pensions/kak_form_bud_pens/).

Since 2015, pensions in the Russian Federation have been calculated in a new way. Now the size of the pension and the right to it depend on the number of points. Let's take a closer look.

The insurance pension (formerly called labor pension) is calculated according to the formula:

number of points * cost of one point.

The cost changes annually and is approved by Government Decree. Those citizens who have earned at least thirty points during their working life have the right to pension provision. The total pension includes the insurance part and a fixed payment (previously the basic part). The size of the fixed payment is also approved at the state level.

That is, only points need to be calculated. And their number depends on the salary.

The first indicator is taken into account in the form of an experience coefficient. It cannot exceed 0.75.

The calculation of average earnings for a pension is made through the “earnings ratio”. This is the ratio of the average monthly salary of a citizen to the average monthly salary in the state for the same time period.

The citizen submitted to the Pension Fund a salary certificate for 60 months from 05/01/1986 to 04/30/1991.

Average earnings when calculating a pension are calculated using the formula:

The average monthly salary in the country is 230.1.

Earnings ratio: 1.2. The law established the maximum threshold for this coefficient: 1.2. Therefore, when assessing pension rights, not 1.38, but 1.2 is taken into account.

How to determine the size of a pension based on average earnings (earnings ratio):

The woman retired in 2015. Total experience – 35 years. Until 2002 – 22 years. This is more than twenty years. This means that the formula for calculating the experience coefficient is as follows:

Let's assume the earnings ratio is 1.2. Since the length of service coefficient is greater than 0.55, the formula for the calculated pension looks like this:

The woman got a job in 1980. Consequently, she has work experience until 1991. When taking into account valorization, it will be necessary to add 10% to the calculated pension and 1% for each full year of work until 1991.

She worked for 11 years from 1980 to 1991.

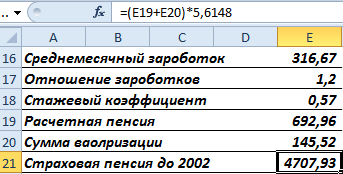

Pension capital is indexed annually. As of December 31, 2014, the index value was 5.6148. Let's find pension rights in rubles for the period before 2002, taking into account bonuses and indexation:

Let's convert it into points. To do this you need to divide by 64.1.

This is part of a citizen's pension rights until 2002. When calculating a pension, the number of points will be multiplied by the value of 1 point accepted on the calculation date.

In other words: the insurance part of a labor pension is a pension calculated according to the “old” rules “minus” the funded part and a fixed additional payment (set by the state).

Calculated for each year of work experience. For the calculation, the salary is taken, on which insurance premiums are calculated. Contributions to the FS – 22%. 16% goes to the formation of the insurance (10%) and funded (6%) part of the old-age labor pension. Let's assume that a citizen does not want to form a funded part separately.

To find the number of points earned in 2015, you need to:

IPCs for different periods are added up and multiplied by the point value accepted at the date of retirement.

This is a simplified calculation without taking into account increasing factors, interrupted service, etc.

Now such a calculation of pensions has been introduced, the calculation formula for which has undergone significant (compared to the previously effective procedure) changes. also made some adjustments. And citizens who independently study the Law “On Insurance Pensions” (where the new formula for calculation was approved) voice a large number of claims. They are faced with difficulties in how to calculate pensions, since the calculation formula does not help.

To understand how pension payments are calculated and what they are, a visit to our website will help. Regarding payment, please refer to the appropriate section. And as usual, the reader can ask the site’s duty lawyer additional questions.

Thus, in 2019, the size of the SPK is 87.24 rubles. From 01/01/2020 – 93 rubles, from 2021 – 98.86 rubles. For more details – 350-FZ dated 10/03/2018.

FV (fixed payment) is established by law and is subject to indexation from February 1 of each year (the Government has the right to index it again from April 1). In 2019, its size is 5,334.19 rubles.

The state will increase the size of the pension fund when the pensioner reaches 80 years of age. Also, when assigning 1st degree disability, those who worked for at least 15-20 years in the regions of the Far North and areas equivalent to the region of the Far North, worked in agriculture.

From 01/01/2019 to 01/01/2025, indexation of fixed payments will not be made. It will be as much as established by Law No. 350-FZ of October 3, 2018. In 2020, the PV will be 5,686.25, in 2021 – 6,044.48. The law established the dimensions until 2024.

The premium coefficient to the fixed payment (KfFV of our formula) is established when delaying the application for an insurance pension. Including .

The Pension Fund applies this coefficient only from 01/01/2015. For example, if it arose on March 2, 2018, and a person applies for it only on March 2, 2019, then for the full 12 months he is set PC 1 in the amount of 1.056. And if 24 months pass, then 1.12. The values of PC 1 are established by the Law “On Insurance Pensions” (Appendix No. 2).

Please note that the mandatory conditions for the appointment of an old-age insurance pension by 2025 will be the presence of 30 pension points, at least 15 years of work experience and reaching retirement age (60 years for women, 65 for men). Since it was adopted by our deputies in 2018.

So, having studied the pension calculation algorithm and the calculation formula, we will give a detailed example of its application.

Citizen of the Russian Federation, born in 1960, reached retirement age 62 in 2022. He did not have the right to a preferential pension. I applied for a pension a year later, in 2023.

Here is the pension calculation:

In 2015, his pension points were converted to 60 points. From 2015 to 2022, he earned another 6 points. In addition, he served, additional IPK 1.8

In total, by addition, we obtain IPC 60+6+1.8 = 67.8.

In total, the amount of the old-age insurance pension for this citizen will be:

FV 6,759.56 rub. (2023) x QEF for 12 months 1.056 + IPC 67.8 x SPK 110.55 (for 2023) = RUB 14,633.38

| Related articles: | |

|

Decorating clothes with flowers, embroidery, beads, rhinestones, accessories, crochet, ribbons, applique

string(10) "error stat" string(10) "error stat" string(10) "error... Simple New Year's toys for a Christmas tree made of paper - ideas for DIY crafts with children Christmas tree with a cardboard ball

The crochet Christmas tree pendant can be crocheted in various colors... Postcard using origami technique “May 9”

Galina Shinaeva On the eve of the wonderful holiday of Victory Day, I propose... | |